- Published on: 26 Oct 2025

- Last updated on: 26 Oct 2025

- Post Views: 4341

-

-

A CIBIL score below 700 often leads to loan application rejection, whereas 720+ boosts the likelihood of approvals. This shows that a CIBIL score matters when applying for a loan. In that, a good CIBIL score matters to improve your chances of successful approval.

Your CIBIL score is one of the most important factors that determines your home, car, or personal loan eligibility. In this blog, we’ll understand why your credit score matters and the tips you can follow to improve your CIBIL score.

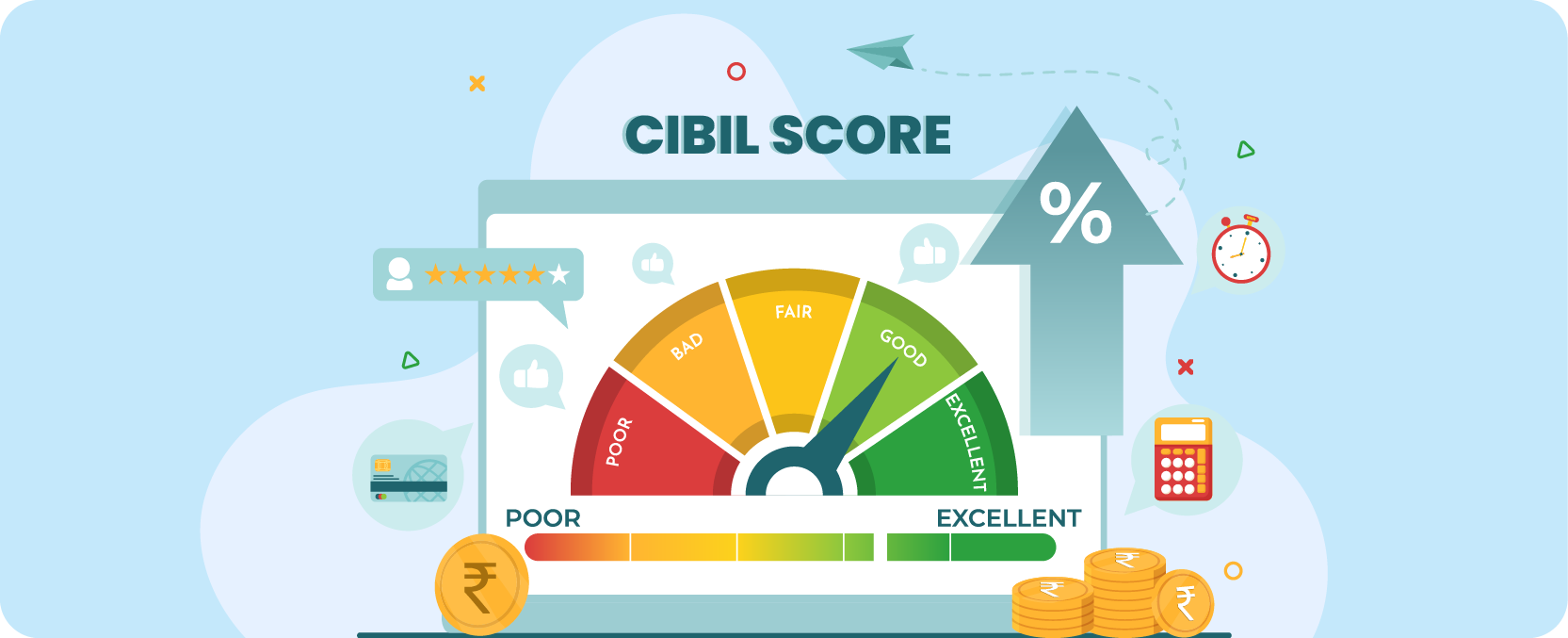

A CIBIL score is a three-digit (Between 300-900) number that indicates your creditworthiness and how well you pay back your credit cards and loans. It usually ranges from 300 to 900, but every range dictates a good or poor standing.

| CIBIL Score Range | What it Means |

| 750-900 | Excellent |

| 700-749 | Good |

| 650-699 | Fair |

| 600-649 | Low |

| Below 600 | Poor |

The higher your CIBIL score, the more reliable and less risky you are to banks and Non-Banking Financial Companies (NBFC). It shows lenders (Banks or NBFCs) that you repay your equated monthly instalment (EMIs) and credit card bills on time and can use credit responsibly.

Here are the different ways having a good CIBIL score will benefit you:

Here are the tips that will help you improve your CIBIL score before applying for any loan:

This is the best method to improve your CIBIL score. When you miss a payment, it shows in your credit report and reduces your CIBIL score. Late payments also indicate that you are not handling your credit properly. To prevent this:

Your CIBIL score will reduce if you use more than 30% of your credit limit. Suppose your credit limit is ₹1,00,000 and you use ₹90,000 every month. Then, in this case, your credit utilisation ratio is 90%, which is too high.

Ideally, you should not use more than 30% of your overall credit limit. If you have a limit of ₹1,00,000, avoid using more than ₹30,000. Keeping your credit utilisation below 30% will increase your CIBIL score.

Every time you apply for a credit card or loan, lenders (Banks or NBFCs) do a hard inquiry on your credit report. Too many hard inquiries in a short span of time can reduce your CIBIL score. If you’ve been denied a credit card or loan, avoid applying for another one right away.

Applying for multiple loans over a short period of time makes you sound credit needy. Wait for at least 3-6 months before you apply for a credit card or loan again. This helps you avoid hard inquiries and improve your credit score.

It’s always a good practice to have a balanced mix of both secured credit (such as a home or car loan) and unsecured credit (such as a personal loan or credit card). If you only have unsecured credit, it might look riskier to lenders.

Having both, on the other hand, indicates you can handle different types of credit responsibly. Avoid applying for unnecessary loans only to increase your credit mix. Instead, aim for a balanced credit portfolio in the long run.

Old credit accounts with a long payment history positively impact your score. If you have an unused old credit card, keep it active, make some transactions, and pay the bill timely. This helps you maintain a strong CIBIL score.

Another way to boost your CIBIL score is by applying for a small personal loan. Consistent EMI payments are reported to the credit reporting companies. Every EMI that you pay without missing adds to your CIBIL score.

CIBIL score is an important aspect of a borrower’s financial history and behaviour. It directly affects your eligibility for a loan. To improve your credit score, you must always repay your credit card bills and loans on time, keep your credit card utilisation ratio below 30%, and avoid applying for too many loans in a short period of time.

At DMI Finance, we do look for a CIBIL score, but we also take into account other factors to approve a loan. We require a CIBIL score of only 700 or higher. Apply for a personal loan of up to ₹5 lakh and get seamless access to it with flexible eligibility criteria.

1. How long does it take to improve my CIBIL score?

It usually takes around 3 to 6 months of consistent on-time payments and balanced credit usage to see noticeable improvement.

2. Will checking my own CIBIL score reduce it?

No, checking your own CIBIL score is considered a soft inquiry and does not affect your score in any way.

3. Can I improve my score if I’ve defaulted on a loan before?

Yes. Repay the pending amount, settle your account as “closed,” and build a new record of timely payments to recover your score.

4. Does increasing my credit card limit help my score?

Yes, it can help as long as you don’t increase your spending. A higher limit lowers your credit utilisation ratio.

5. How do I correct errors in my CIBIL report?

You must raise a dispute on the official CIBIL website by submitting proof of the error. The correction usually takes 30–45 days.

6. Will closing unused credit cards improve my CIBIL score?

No. Closing old cards can shorten your credit history and reduce your CIBIL score.

7. Can a co-applicant’s low score affect my loan approval?

Yes. If you apply jointly, lenders consider both scores, and a low score from one applicant can reduce approval chances.

8. What should I do if I don’t have any credit history at all?

Start with a small personal loan or a credit card and make regular payments without delays to build your score.

9. Does paying only the minimum due on my credit card hurt my score?

Yes. Paying just the minimum keeps your balance high and increases interest, which can lower your score over time.

10. Will becoming a loan guarantor affect my CIBIL score?

Yes. If the borrower defaults, it will appear in your credit report too and can hurt your score.